An Overview Of The Issues & Suggestions About Sec 146 Of The Patents Act, 1970 And Form 27

- Apr 13, 2018

- 2 min read

As a result to the PIL filed by Prof. Shamnad Basheer, complaining against IPO for noncompliance of section 146 (working statement of Patent invention), in the year 2015, the Delhi High Court, recently in January 2018, passed an order directing the Government to submit an affidavit outlining a plan for putting in place a standard operating procedure/enforcement mechanism with respect to Form 27 as well as taking an action against errant patentees. With respect to this, the Patent Office invited the stakeholders to come up with their suggestions for making Section 146 and Form 27 effective.

The IP India portal has provided with suggestions provided by various organizations (here and here), few of which has been majorly discussed by most of the stakeholders as provided below:-

One Form One Patent: The first and foremost issue that most of the stakeholders such as Dr. S.K. Murthy Core-Committee Member, In-House IP professionals (IHIPP) forum, DR. P. Ganguly Vision- IPR (Patent Professional Firm), Federation of Indian Chambers of Commerce and Industry(FICCI) raised was the provision of submitting different forms for different Patents. Most of the organizations are with a view that bringing in a single form for multiple Patents would fulfil the business objectives of the present world.

One Product One Patent: Many stakeholders including S.S. Rana & Co., Singh & Singh Law Firm LLP which pointed out that presently, Form 27 runs on the presumption that one product is equivalent to one patent, which is not the case with many industries where one product is not based on one patent but is actually covered in portfolio of patents and such portfolios are owned by different Patentees. S. Majumdar & Co, an IPR Firm based in Kolkata mentioned that there are many cases especially in FMCG industries, Information and Communication Technology, semi- conductors, Electronic companies, etc, where one product is equivalent to various Patents. Therefore, It is suggested that form 27 may allow patentees to make a statement to the effect that Patent is not worked in a standalone format but form a part of the portfolio licensing program. H. K. Acharya & Company, an IPR Agent firm suggested that it would be sufficient to provide information about product in which the Patented product/process is used rather than providing all the technologies, applications and product where the patent is so deployed or used. Dr. Shital Chopra ASSOCHAM suggested that the forms should provide single statements for multiple Patents, specifying single Patent forms a part of the portfolio license.

Quantum Valuation: De Penning & De Penning, Federation of Indian Chambers of Commerce and Industry, IPR International Services, KRISHNA & SAURASTRI ASSOCIATES and others observed that Form 27 has nowhere described the method of calculating sales and commercial use of Patents, it becomes difficult to calculate the value of Patent in the market because of various confusion such as whether taxes is to be included or not or whether the end product is to be valued, etc. While recommendations from Federation of Indian Chambers of Commerce and Industry, Huawei Technologies Co Ltd, China emphasized that provision of submitting such quantum and valuation' should be removed, there were few stakeholders such as Bosch Group of Companies, CIPA Patents Committee, Chartered Institute of Patent Attorneys (‘CIPA’), London and Hindustan Unilever Ltd., Lal Lahiri and Salhotra, which showed their concerns over the same and have expressed its interest in a guidance notice in order to clarify on how to ascertain the quantum.

Simple, Clear and Unambiguous: Few Academicians such as Raj S. Davé IPR Chair Professor for Excellence at Gujarat National Law University and Justice Asok Ganguly, Former Supreme Court Justice of India and Adjunct Professor at Gujarat National Law University, Prof. Shamnad Bashir ,Nirma University Pankhuri Agarwal, reseach associate N. Sai Vinod, Advocate along with Hrishikesh Raychaudhury Corporate Law Group , Singh & Singh Law Firm LLP and other stakeholders pointed out that the existing Form is ambiguous regarding the information related to the commercial scale, scope of public requirement, disclosures and reasonable price etc. It is requested to make it simple, clear and unambiguous and limit it to statutory requirements that has to be met, which is 'whether the Patent has been worked or not.'

Information regarding Manufacturing in India and Imported to India: The current form is concerned with the information regarding 'working of Patent in India', however, nowhere in the Act, the term 'working Patent' has been defined. Obhan & Associates, KRISHNA & SAURASTRI ASSOCIATES and ALG India Law Offices LLP highlights that there exists an ambiguity with respect to the term 'working' which may or may not involve manufacturing in India, the quantum value of production of products sold in India or for only exporting purpose. It is suggested that the Act must clearly explain as to 'what is working Patent' and is also recommended that 'Working Patent' must be limited to India as far as it meets the public requirement. Huawei Technologies Co Ltd, China interprets the IPAB decision of Bayer Corporation v. Union of India and Article 27(1) of TRIPS agreement and identifies that the term 'working' may include importation.

Frequency of Form of Submission: According to Section 146 of Act, information regarding the working Patent is to be submitted annually, with intervals not being less than six months apart. Therefore, this increases the burden on the Patent office as well as the Patentees and it is also difficult to collect the relevant information on such a frequent basis. The same issue was brought forth by Eri Honda(Ms.) Corporate Intellectual Property and Legal Headquarters Canon Inc., Japan, Japan Pharmaceutical Manufacturers Association, Japan, Remfry & Sagar and Obhan & Associates. It is pertinent to note that most of these stake holder have suggested to reduce the frequency of submitting a statement to once in every three years.

Confidentiality: Most of the stakeholders such as In-House IP professionals (IHIPP) forum, Anand & Anand, K&S Partners, Lexorbis IP Attorneys etc, are concerned about disclosing the confidential information related to their licensees and other related data due to the requirement of the publication of the submitted information. SKS LAW ASSOCIATES went ahead and noted that such provision/practice is not business savvy. Further, Singh & Singh Law Firm LLP highlighted that such disclosure of information is also contrary to section 62 of the Patent Act which provides for an opportunity to the Patentee to request the Controller to not to disclose the information to anyone except the order of the Court. Moreover, on a careful perusal of Section 146(3) r/w Rule 131(3), it can be observed that the use of the word "may" in the provision, puts a discretionary power on the controller to disclose the information or not. However, the Controller is required to apply his mind while practicing the discretion vestedin These stakeholders also Laxmikumaran & Srihdaran mentioned that provision for providing such information may be retained, however, the disclosure of such statements must be done away with.

Exemption from Form 27: while deliberations for modifying Form 27 was going on, few of the stakeholder also suggested to give exemption from submitting Form 27 for the first three years of the patent issued because the statutory limit for compulsory licensing is three years.

Penalties: Section 122 provides for penalty for not complying Form to 27. Such penalty includes imprisonment as well, which is believed to be harsh. Thus, stake holders like Hindustan uniliver or Industries in association with USA (Global Innovation Policy Center (GIPC) and U.S.- India Business Council (USIBC)), have suggested to strikeout such penalty for failing to provide working statement. Moreover, IP firm Remfry and Sagar, came up with a view that compulsory licensing as a penalty for non-compliance of provision would be enough for deterring the errant Patentee. However, there are few that stakeholders like who strongly support the said provision with a view that striking off of criminal penalty would dilute the system leading to its rampant misuse.

Miscellaneous: There are suggestions like removal of sec 146 and rule 131 completely, in order to ease the business of Industries. where digitalization is taking over the world and most of the most important work can be done through internet. It is recommended to digitalise the form in order to make it convenient for the Patentee to submit the Form.

It is incredible to note that the stakeholders were also as much a part of this process as the Government. As much as 64 stakeholders came forward with various issues with regard to Form 27 and its solutions. Stakeholders included major key players in the market such as Bosche, Japanese IP Group, FICCI, Huawei Technologies Co Ltd, China, CIPI, London and many more. There were other responsible academicians from various Law universities and the rest were Intellectual Property Firms such as Lexorbis, Anand and Anand, S.S Rana and others.

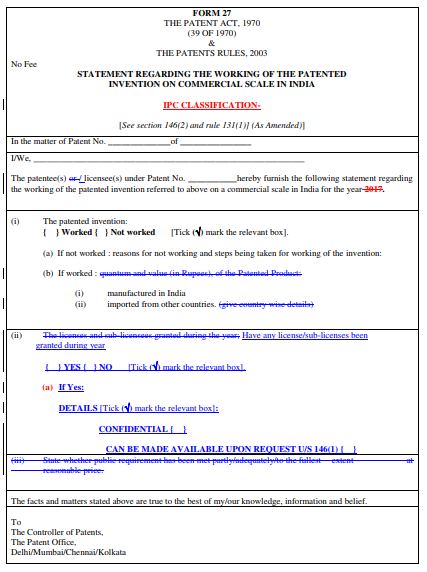

The above mentioned are the few suggestions to the issues that have been recommended by majority of Organizations. It can be observed that Form 27 needs to be a little flexible with the changing dynamics of Industries of the Contemporary practices. Also, the Act needs to be more clear about its provisions and explanations with respect to 'Working Patent' , 'disclosure of information' and frequency of submission of Form 27. This would not only make the procedure smoother for the Patentee, but would also help the Patent Offices to function swiftly. The proposed revised form may be something like as provided below.

Author: Pratistha Sinha, Associate, Yogita Shinde, Intern and Mudiganti Sai Krupa, Intern at Khurana & Khurana, Advocates and IP Attorneys. In case of any queries please contact/write back to us at swapnils@khuranaandkhurana.com.

Comments